Cost Sharing Among State Defined Benefit Pension Plans

The rotunda of the Oregon State Capitol.

Connecting state and local government leaders

In response to the budget strains and funding challenges, some states have looked to alternatives to traditional pensions.

This article was originally published by Public Retirement Systems, an initiative of The Pew Charitable Trusts, and was written by Greg Mennis.

A number of states with defined benefit, or traditional, pension plans have enacted policies that retain the core elements of the plans while sharing the risk of cost increases—as well as potential gains—between public employees and employers. These mechanisms for sharing costs can help reduce volatility and investment uncertainty while preserving the ability to pay promised pension benefits.

For most public sector defined benefit (DB) plans, the cost of providing these benefits fluctuates, depending on investment performance, inflation, salary growth, life spans, and workforce demographics. Cost volatility can strain state or local budgets or lead to underfunded pension plans if policymakers have not provided sufficient contributions.

In response to the budget strains and funding challenges, some states have looked to alternatives to traditional pensions, including defined contribution, cash balance, and hybrid plans. Still, most state and local governments continue to offer DB plans, though many now use cost-sharing mechanisms to reduce budget uncertainty. Employees continue to receive guaranteed lifetime benefits and in some cases see gains, such as higher cost of living adjustments (COLAs), from strong investment returns.

A formal cost-sharing policy distributes unexpected cost increases—costs that result from short- or long-term deviations from plan expectations—between employers and employees. Typically, the process is codified in state statute or policy, is transparent, and is set in motion by either investment returns or plan funding levels.

Approaches can include splitting some or all of the plan costs between the employer and the employee, or adjusting the employee contribution in response to investment returns. Alternatively, cost-sharing policies can modify COLAs or post-retirement benefit increases based on investment returns.

Further details on the 28 defined benefit plans in 16 states that use formal cost-sharing mechanisms to manage risk can be found in The Pew Charitable Trusts’ report Cost Sharing Features of State Defined Benefit Pension Plans.

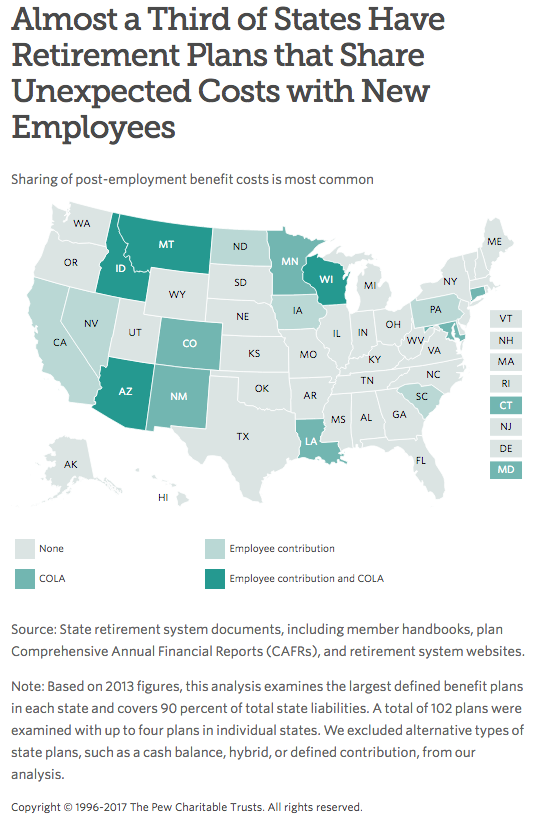

This map and table highlight strategies used by large state pension plans to share cost increases with members. Looking at the benefits offered to new workers in 102 primary state retirement plans, Pew’s public sector retirement systems project identified 28 plans in 16 states that use formal cost-sharing mechanisms to manage risk.

Note: Based on 2013 figures, this analysis examines the largest defined benefit plans in each state and covers 90 percent of total state liabilities. A total of 102 plans were examined with up to four plans in individual states. We excluded alternative types of state plans, such as a cash balance, hybrid, or defined contribution, from our analysis.

Read more about the various types of cost-sharing plans used by state governments around the country.

NEXT STORY: Relative of Kansas Gov. Slams His Budget Proposal; Colo. Lawmakers May Pursue Tax Hike