Indiana’s Medicaid Experiment May Reveal Obamacare’s Future

Nearly 20 governors turned away the federal funding to expand Medicaid offered under the Affordable Care Act. But Mike Pence, governor of Indiana, was not one of them.

Connecting state and local government leaders

The state’s health-care system was expanded under the Affordable Care Act. Now, it may serve as a model nationwide.

INDIANAPOLIS—Nearly 20 governors turned away the federal funding to expand Medicaid offered under the Affordable Care Act. Their states’ opposition to Obamacare meant that tens of thousands of low-income people in their states continued to live without health insurance.

But Mike Pence, governor of Indiana, was not one of them.

After two years of negotiation, Pence in January 2015 reached an agreement with the Obama administration granting Indiana a waiver to try its own form of Medicaid expansion, called Healthy Indiana Plan (HIP) 2.0. The state would become one of the 31 that participated in the Medicaid expansion, receiving federal money through the Affordable Care Act to cover people between 100 percent and 138 percent of the federal poverty line. (Medicaid already covered a limited number of people living below the poverty line.) But it could also add its own modifications, the most salient being that participants would be required to contribute monthly fees to continue to receive access to health care.

“The good news is that Indiana is a state that bought into Obamacare,” Joan Alker, a Georgetown professor who is the executive director of the Center for Children and Families, told me. “The bad news is that Pence’s vision of coverage has a lot of barriers.”

Indiana’s Medicaid expansion, with its requirement that poor people contribute to savings accounts which are then applied to the portion of the bill that insurance covers (not the co-pay), could be a model for how the Trump administration structures health care for low-income people across the country. Its architect, Seema Verma, has been appointed head of the Centers for Medicare and Medicaid Services by the Trump administration. Trump says he wants to give states more control over how they run Medicaid, and also that he wants to push health-savings accounts similar to the ones the poor pay into in Indiana. Already, other states, including Kentucky, are appealing to the federal government to be allowed to copy parts of the Indiana plan.

Yet Indiana’s is a complicated way to get health insurance to people, and could change the lives of the 11 million people who have benefited from the Medicaid expansion. At stake is the historic decline in the uninsured rate among non-elderly people in the U.S., which fell to 10 percent in 2016 from 16.6 percent in 2013.

HIP 2.0 works like this: People living at between 100 percent and 138 percent of the federal poverty level (roughly between $12,000 and $16,000 annually for an individual and between $24,000 and $33,500 for a family of four) must pay a monthly fee into what’s called a POWER account. This qualifies them for a plan called HIP Plus, which includes dental and vision care and has no co-pays unless people visit the ER unnecessarily. These contributions amount to about 2 percent of their income, which is about $27 a month for a person earning $16,000 and $55 for a family of four earning $33,500. HIP then uses the money in the POWER account to pay for covered services (not co-pays, which must be paid out of pocket). Should people fail to pay the monthly contribution, they lose their health insurance and are locked out of re-applying for coverage for six months. People below the poverty line are on something called HIP Basic, which excludes dental and vision, and requires hefty co-pays. They’re also encouraged to pay a monthly premium into and get on HIP Plus. If they neglect to pay the premium, they get knocked back down to HIP Basic.

With HIP 2.0, “there are more costs for low-income families and individuals,” Alker said. “That means they may miss the care that they need.”

A study from the liberal think tank the Center on Budget and Policy Priorities (CBPP), found that because of the premiums required, one-third of eligible individuals who apply are not enrolled because they haven’t made a premium payment. Around 30,000 people, the study found, had been found eligible in the past 60 days but hadn’t enrolled at all. “HIP 2.0’s premiums are deterring significant numbers of eligible low-income people from enrolling,” the report concluded. For many people, the cost wasn’t the biggest obstacle. Rather, 84 percent of people who were bumped from HIP Plus to HIP Basic for nonpayment said they had been confused about the payment process and the program in general.

Diana Goodman, 62, a resident of Bloomington, lost her HIP Plus coverage after she forgot to pay her monthly premium for a few months (she isn’t sure how many). Goodman, a landscaper, hadn’t had health insurance in decades when she signed up for HIP Plus. The paperwork and monthly payment were complicated, though, and she neglected to pay. “It’s not so much the amount each month, it’s remembering to do it,” she told me. After she lost health insurance, she couldn’t go to the dentist or to the eye doctor, which she had been hoping to do since she had been wearing glasses with the wrong prescription for years. Now she’s back on HIP Plus, and has already made appointments with the eye doctor and dentist. But she’s paranoid that she’ll forget to pay the bill—one of many she deals with—and lose the additions to her basic coverage again.

“The lock-out issue is very important and problematic,” Alker said. “Forcing people to remain uncovered … seems a high price to pay.”

HIP 2.0 also seeks to encourage “personal responsibility,” a perennial conservative-policy favorite. Enrollees who seek preventative care—thus demonstrating personal responsibility—can receive reductions in future premiums. Yet the CBPP report suggests that few people receive these reductions because they don’t know how those premiums work and don’t seek the preventative care as a result.

Still, health-care advocates in Indiana say that a Medicaid expansion with hoops to jump through is better than no Medicaid expansion at all. Hundreds of thousands of people now receive some sort of coverage who had none before. By October of this year, 419,369 people in Indiana had enrolled in HIP Plus, up from the 40,000 who had incomes low enough to receive coverage before the Medicaid expansion, according to Kosali Simon, a professor at Indiana University-Bloomington who has been studying the expansion. That’s 73 percent of all those who were considered eligible when the expansion was announced.

“It’s the best thing that’s happened to us,” Susan Jo Thomas, the executive director of Covering Kids and Families of Indiana, told me. “It’s going to be a very sad day if there’s a rollback or there isn’t continued support.”

And some preliminary evidence suggests that most people are able to keep paying into their POWER accounts. An independent evaluation of the first year of the Medicaid expansion in Indiana found that 90 percent of HIP Plus members were able to make contributions to POWER accounts and remain in HIP Plus. Only eight percent of members who had made at least one contribution to their POWER account failed to continue to make a payment and were moved to HIP Basic, the report found.

Many providers in Indiana told me of people who had never had health insurance and who finally were able to see a doctor. “People are actually reaching out and accessing care,” Jean Scallon, the CEO of Bloomington Meadows Hospital, told me. “They’re not waiting until they are ill or potentially out of medication.”

Before the expansion, Indiana had a plan called HIP, but without funding, it didn’t serve many people. There were long waiting lists and only very, very poor people and children were able to get coverage. Thomas says her staff would often talk to people seeing coverage, only to turn them away, telling them they “weren’t poor enough” to qualify. “We have lots and lots of people who never went to the doctor, that never even considered it as an option, and literally lived sick for years,” Thomas said.

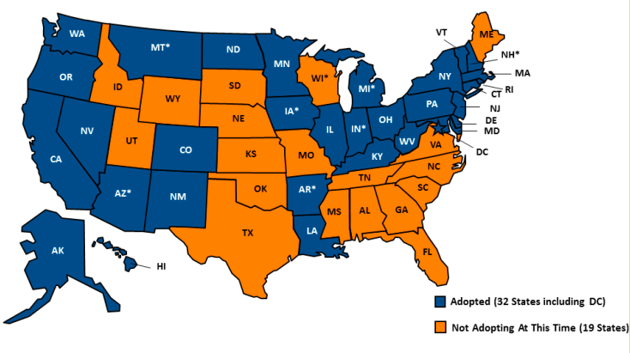

Status of the Medicaid Expansion, by State

Julia Holloway, the project director of ASPIN Health Navigator, which signs up people for HIP Plus and the insurance marketplace, told me her organization enrolled a homeless man who had a broken bone in his hand that he hadn’t realized was broken. Once his chronic pain was addressed, he was able to seek employment. Goodman, the landscaper, said going to the doctor was a completely different experience once she had health insurance. “I feel like I am being treated like a real person and not some poor person,” she said. “If you don’t have the money, the good insurance, you may just get put in the room and not checked out.”

I also talked to a man named Fritz Harbridge who had been unemployed when he went into a free clinic to get a physical and found out he had a tumor in his neck. Because he was able to get on HIP Plus, Harbridge, 52, was able to have the tumor removed and undergo cancer treatment. Without the expansion, he said, “likely I would have exhausted every resource that I have, and likely still would have had to go so far into debt” to get care, he said. “It’s almost unfathomable at this point to consider. I think my outcome would have been significantly different health-wise.”

Many people are worried that under the Trump administration, the country could return to that “unfathomable” state in which poor people can’t afford health insurance, and thus can’t get treatment. After all, Donald Trump has pledged to repeal Obamacare, and his pick for Secretary of Health and Human Services, Representative Tom Price, is a vocal opponent of the Affordable Care Act. A repeal of Obamacare would also mean that the funding for the Medicaid expansion disappears—one of the biggest tenets of Obamacare, after all, was the Medicaid expansion, and Trump has said he will ask Congress to deliver a “full repeal” of the Affordable Care Act on his first day in office. He has also said he supports a proposal by Speaker Paul Ryan to give Medicaid funding to the states and let them decide how to administer the program. The Center for Budget and Policy Priorities says that administering the program in this way, also called a block grant, would cut federal funding for Medicaid by one-third.

Even if the Trump administration somehow keeps the Medicaid expansion, experts say, the poor in states like Indiana could see access to health care diminished. That’s because the waiver granted to the state has provisions that the Obama administration insisted upon, provisions that a Trump administration may not care about. The state wanted the lowest monthly payment to be $3, the Obama administration insisted upon $1, according to the Indy Star. The administration was also able to ensure that some “frail” or unhealthy people would not be locked out of health insurance if they failed to pay their premium. The Obama administration also insisted that people below the poverty level could not get kicked off of health care entirely, Alker said.

In the end, Indiana may be used as an example by the Trump administration of how to allow people to access health care while not giving “a handout” without participants’ contributions.

HIP 2.0 is “intended to be a safety net that aligns incentives with human aspirations,” Mike Pence said, about the program. Any safety net is better than no safety net at all, of course. But the experience of people on the program challenges the assertion that it’s better than the Medicaid expansion other states have implemented, which have fewer rules and lower barriers to coverage.

Alana Semuels is a staff writer at The Atlantic, where this piece was originally published.

NEXT STORY: Illinois maps its smart state transformation