'Risk Is Shifting' for State and Local Employees Planning for Retirement

The Adam Clayton Powell, Jr. State Office Building in New York City Shutterstock

The changes are taking place in an era when some state and local governments are struggling with pension costs.

WASHINGTON — State and local public employees around the U.S. are bearing increased risks and experiencing less certainty when it comes to the security of their retirement benefits.

During the last two decades, state governments have sought to restructure public employee retirement systems, often with an eye toward decreasing pressure on their budgets. The trend has taken place as some states and localities are grappling with how to cover the heavy cost of promised pension benefits for retired public workers.

Those affected by the changing retiree benefit landscape include employees like teachers and firefighters.

“In general, risk is shifting,” said Keith Brainard, research director for the National Association of State Retirement Administrators. “A generation ago, the employer was bearing all of the retirement risk—inflation, investment, longevity.”

There are some ways, he said, that newer retirement plan designs could provide advantages to employees. “But predominantly it is on the downside,” Brainard added. “It’s a lower benefit.”

Brainard made his remarks at an event here Monday focused on retirement issues that was held by the Center for State and Local Government Excellence.

A major change he pointed to is the movement away from “defined benefit” pension plans.

These are programs where employees, when they reach a certain age and number of years of employment, are eligible for a guaranteed monthly benefit based on their salary and the length of time they have worked. With traditional defined benefit pension plans, benefits can not be outlived and last until a retiree dies.

On the other end of the spectrum are “defined contribution” plans, where an employer provides a retirement savings program employees can put their money into. The employer usually contributes to employees' accounts as well. A popular example would be a 401(k).

In between are “hybrid plans." These commonly feature a defined benefit plan that provides a lower benefit than a traditional pension, combined with a defined contribution program.

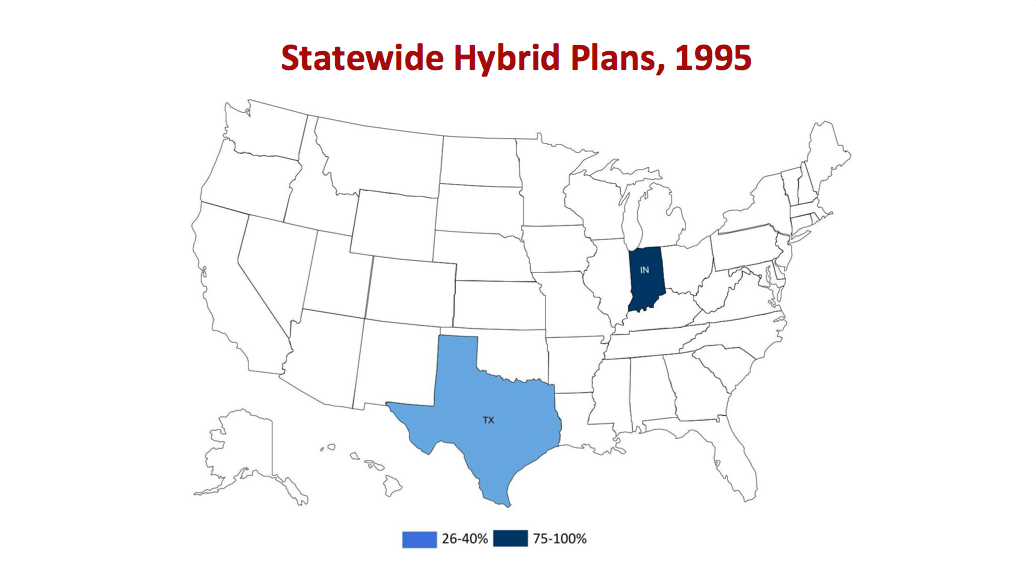

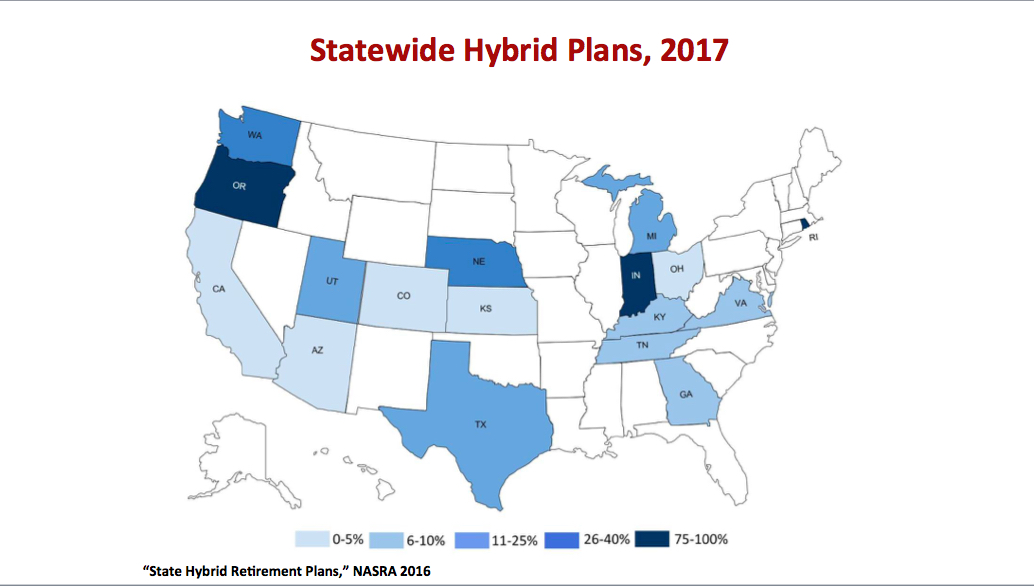

Brainard noted that in 1995 there were just two states, Texas and Indiana, with statewide hybrid plans for some or most public employees. By this year, that figure has increased to 17 states.

“It really is a dramatic change,” Brainard said.

In most instances, these hybrid plans are optional or apply only to new hires, while employees hired in earlier years remain eligible for traditional, defined benefit pension programs.

The number of states with optional or mandatory defined contribution plans has also grown, according to Brainard.

While decreased enrollment in defined benefit plans might ease strain on a state’s finances, it can also mean less certainty about the level of benefits public workers will receive after they’ve retired.

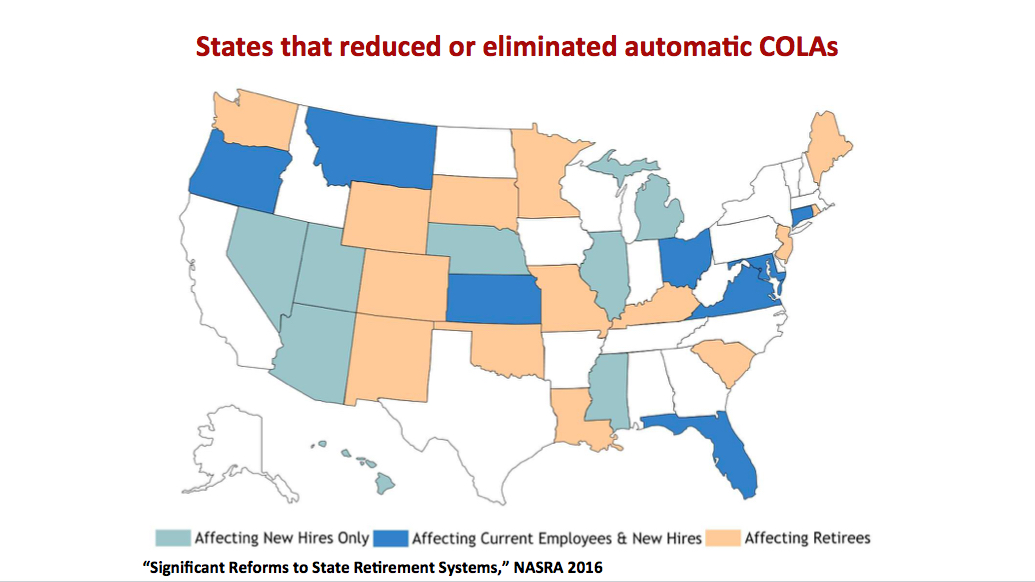

Brainard flagged other trends as well that could increase the uncertainty state and local government employees face when it comes to the retirement benefits they will receive.

One is the reduction or elimination of automatic cost-of-living adjustments, which increase the benefits that an employee receives gradually to keep pace with inflation.

Another concerns “triggers” to close retirement plans if the money available to cover benefits dips below a certain level in consecutive years. Michigan, for example, recently introduced changes like this that will affect teachers hired beginning in February of 2018.

Flexible, as opposed to fixed, employee contribution levels to plans can also create risks for retirees, Brainard said.

Shane Cochran is division chief for program implementation for the Office of Housing in Alexandria, Virginia and chair of the city’s Supplemental Retirement Board.

He explained Monday that the Virginia Retirement System has transitioned to a hybrid plan for recent hires. The city, meanwhile, has limited lump sum payouts under its supplemental plan.

“Changes seem to be the constant at this point,” Cochran said.

He later added that by enrolling new workers in different benefit programs than those hired in past years it can lead to a system where there are “tiers of employees with different benefit levels.”

“I think that creates a little bit of tension,” he said. "New hires are probably, hopefully, negotiating higher salaries to cover some of those costs. I'm not sure that's the case."

Al Tierney, a retired police officer from Alexandria, Virginia said police and firefighters tend to be more vocal than other public employees about unwanted changes to their pensions.

“If we don’t like the deal,” he said, “we'll knock on the mayor’s door and say ‘we don’t like the deal.’”

Bill Lucia is a Senior Reporter for Government Executive’s Route Fifty and is based in Washington, D.C.

NEXT STORY: Local Government Officials Buck ‘Big Six’ Tax Reform at the Expense of SALT