‘Progressive’ Tax on Inherited Wealth Could Net 33 States as Much as $6.1B

New York currently makes the most off its estate tax, but California has the most to gain, a liberal policy group argues.

State policymakers should consider adopting taxes on inherited wealth as a way to lessen the tax burden on people with moderate incomes and allow them to spend more in local economies, a new Center on Budget and Policy Priorities issue brief argues.

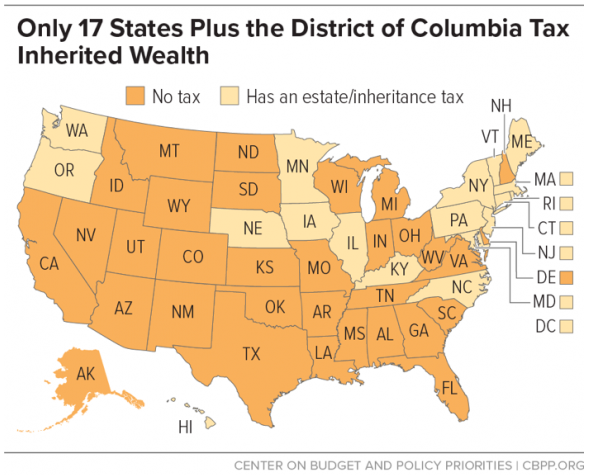

Thirty-three states have no taxes on inherited wealth. The liberal-leaning CBPP says that more should re-examine that policy, saying this would help make local and state tax structures more progressive.

Estate and inheritance taxes are a big point of contention in the debate about how best to set up tax structures, with the conservative-leaning Tax Foundation earlier this year saying they are “burdensome and disincentivize business investment.” For those that continue, the foundation urges them to adopt the new federal policy embraced in last year’s tax cut policy of exempting up to $11.2 million per person.

An estate tax is a tax on assets transferred from the deceased to any heir other than a spouse, if the cumulative value exceeds a certain threshold. Of the states that have a tax, most exempt $2 million to $5 million and tax at a rate between 1 and 16 percent, according to CBPP, with fewer than 3 percent of estates affected.

Alternatively, states may levy an inheritance tax on estate recipients, rather than the estate itself. Maryland is the only state with both an inheritance and estate tax, according to the Tax Foundation.

In 2001, lawmakers cut the federal estate tax and ended a dollar-for-dollar credit estates received for paying state estate taxes, creating a patchwork of responses. As a result, only 17 states and Washington, D.C. currently levy an estate or inheritance tax to the tune of $4.5 billion annually, according to the brief, but that number could increase as much as $6.1 billion if the other 33 followed suit.

“Cuts in state services resulting from eliminating the tax can discourage businesses and individuals—both retirees and others—from remaining in or relocating to a state, likely doing more harm to the state’s economic growth than any small potential benefit from having no estate or inheritance tax,” reads the report.

CBPP advises states to maintain their estate or inheritance taxes by enacting policies like unlinking them from the federal estate tax exemption, which cuts into their revenues when increased.

States without such a tax could re-establish one at the same level as the federal credit before it was ended in 2001, though that limits flexibility, or adopt a standalone tax disconnected from federal estate law.

In California, residents must vote to restore the estate tax, and Alabama, Florida and Nevada still limit the size of a potential estate tax.

A third, “progressive” option proposed by CBPP would tax some or all of an inheritance as income with wealthier heirs paying a higher rate.

In 2017, New York collected the most estate-inheritance tax revenue to the tune of $1.1 billion, while Delaware collected the least at an estimated $5 million.

Of the states without such taxes, California has the most to gain by reimplementing one: $1.7 billion assuming only a $1 million exemption and almost $1 billion if the exemption was as high as $5.43 million for each estate. Alaska, North Dakota and South Dakota could collect about $10 million each with an estate tax with the $1 million exemption.

Dave Nyczepir is a News Editor at Government Executive’s Route Fifty and is based in Washington, D.C.

NEXT STORY: Federal Watchdog Offers Gloomy Outlook for State and Local Budgets