California Now Prohibits Use of Gender in Determining Auto Insurance Rates

A driver for a car service in New York City that caters to women riders with women drivers. AP Photo

Connecting state and local government leaders

Studies show that women often pay more than men for auto insurance.

This story was originally published by Stateline, an initiative of The Pew Charitable Trusts.

It’s a widespread belief that men pay more for automobile insurance than women. But that’s only true for young adults.

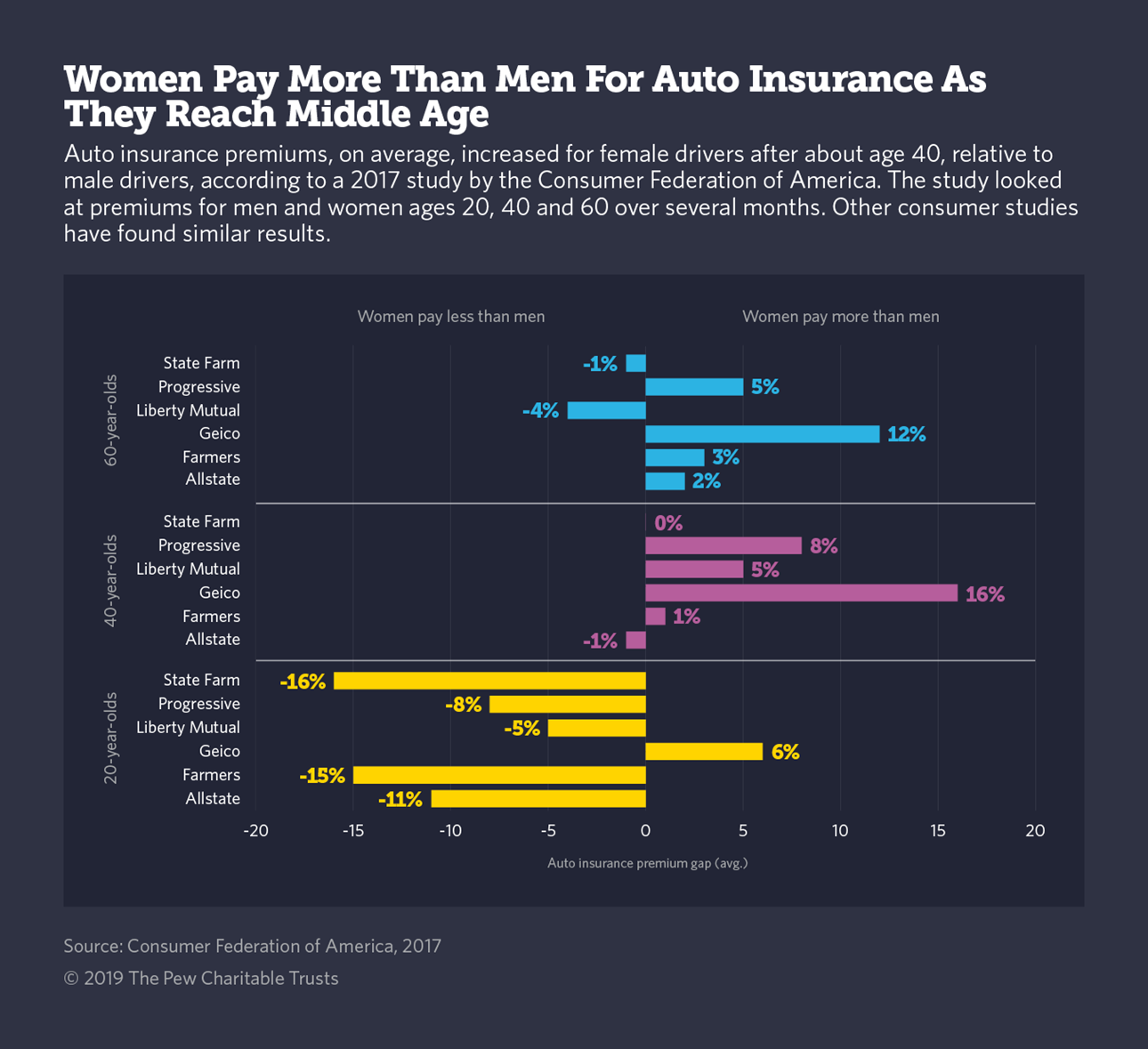

Several studies in 2018 and 2017 revealed that women over 25, particularly those between 40 and 60, often pay more than men—not less—for auto insurance, all other rating criteria being equal. Now, California has become the latest in a handful of states that have outlawed setting rates for automobile insurance based on gender.

As one of his last acts before leaving office at the end of 2018, former California Insurance Commissioner Dave Jones issued regulations prohibiting the use of gender in individual automobile insurance ratings in California, effective Jan. 1.

California is the first state in decades to take the step, joining states including Massachusetts, Michigan, Montana, North Carolina and Pennsylvania, most of which passed their laws in the 1970s and 1980s in the wake of the women’s rights movement.

In an interview, Jones said it’s fair for insurance companies to set premiums based on a driver’s accident history, number of speeding tickets and other factors that are under the driver’s control. But using gender is unfair because a person has no control over that, he said.

“An internal analysis by the department concluded auto insurers in California were all over the map with regard to how they handled gender as a rating factor,” Jones said. “In some cases, women were paying more and some less than similarly situated men. There was no consistency.”

Why? The insurance industry won’t give many reasons.

Several insurance companies contacted by Stateline, including Geico, Farmers and Progressive, refused to comment for this story or to explain what factors they consider in setting rates, including gender.

A spokesman for Farmers referred inquiries to a trade group, the Insurance Information Institute.

Janet Ruiz, the group’s spokeswoman who is based in California, said auto insurers in the state use many criteria in setting rates, and prior to the new regulation, gender was a “minor” one. She predicted there would not be a big difference in rates for men or women because gender “doesn’t have much weight in the pricing overall,” adding that rates might go up or down by about $25 a year.

Ruiz said she disagreed with a 2017 analysis by the Consumer Federation of America showing women nationwide often are charged more, but she could not provide numbers that would counter the report. Another industry trade group suggested that banning gender discrimination could hurt competitive pricing.

“The auto insurance marketplace is highly competitive,” said Maggie Seidel, vice president of public affairs for the American Property Casualty Insurance Association. “When you eliminate rating factors it cuts back on choices that consumers and insurers may want.”

In comments presented to the California Department of Insurance, the state chapter of the American Property Casualty Insurance Association argued that gender rating has been used for nearly 30 years in the state and is “based on actuarially sound principles” and “gender statistics.” For example, men drive more miles than women, and teenage male drivers present higher risks than teenage female drivers.

“We are concerned that this proposed change would limit carriers’ ability to price the insurance risk accurately, causing some consumers to have to start paying higher rates than they would otherwise,” the group said in a written response to the new rules.

But a professor at University of Minnesota Law School, Daniel Schwarcz, said if companies are not allowed to use “outdated stereotypes based on generalities” about men and women, the insurers will have to consider “more directly” such measures as the actual number of miles driven, the number of years customers have been driving and where they live.

Insurance companies have until June 30 to submit new ratings plans, with the gender factor eliminated, for approval by the California Department of Insurance, now headed by Ricardo Lara.

Several studies have documented that women often pay more for automobile insurance than men, in addition to the one by the California Department of Insurance, including studies by the Consumer Federation of America, Texas Appleseed and the Michigan Coalition Protecting Auto No-Fault.

According to the 2017 Consumer Federation study, 40- and 60-year-old women with perfect driving records were charged more than men for basic coverage nearly twice as often as men were charged the higher rate. Even when looking at young drivers, a time when men have more accidents, premiums were lower for women only some of the time, the study found.

The study also polled U.S. drivers. Forty-eight percent said they thought men pay at least as much as women for automobile insurance. Only 23 percent said they thought women pay more than men.

The 2018 study by Texas Appleseed, a public interest organization, found that women in Texas paid $56 more a year, on average, than men for auto insurance that satisfies the minimum required by law. Single and divorced women paid an even higher premium: $80 more a year, on average, than similarly situated men.

The Consumer Federation’s Douglas Heller, an insurance expert who worked with the group on the studies, said teenage male drivers usually pay more or about the same as teenage girls. But as they grow older, the women start to pay more, he said, in some cases much more.

Heller said his study found that nationwide, many women were paying hundreds of dollars more in premiums and “in several cases, they were paying $500 more for no reason other than they marked the ‘F’ under gender. That was stunning to us.”

California’s new insurance commissioner, Lara, acknowledged that some drivers might see their rates change as a result of the anti-discrimination policy, especially new drivers.

“But those changes even out as you gain more driving experience,” he said in an email. “With approximately 170 companies licensed to sell private passenger auto insurance here, there will be a lot of variation and choice for drivers.

“We will be watching insurers closely,” Lara said, “and we expect all these changes to be revenue neutral—no insurance company is going to make more money under a gender-neutral policy.”

Part of the reason automobile insurance is so competitive is that every state but New Hampshire requires drivers to have at least enough insurance to cover their liability in an accident. Or they can put up a bond.

Because the laws give insurance companies a captive audience, it’s by offering lower prices and more coverage that companies hope to attract a larger share of the market.

Schwarcz, who has written about insurance and discrimination, said insurers use varying models to price risk.

“They are going to have a particular subset of policyholders and make decisions based on that,” he said. “Sex has been something that insurers can discriminate on. I don’t think we have a comprehensive sense of exactly how prevalent that phenomenon is.”

But, Schwarcz said, Californians should not expect to see major changes in their auto insurance premiums.

“In most cases, the conventional wisdom is that it’s not going to make a huge [price] difference,” he said. “That’s not what’s been driving pricing in California. That doesn’t mean we shouldn’t regulate it, but it’s unlikely we’re going to see a substantial change in the marketplace.”

In a 2014 paper, “Understanding Insurance Anti-Discrimination Laws,” Schwarcz and his co-authors noted that state laws against insurance discrimination generally cover race, national origin, religion, sexual orientation and genetics. The laws generally do allow factoring in gender, age, credit score and ZIP code.

In Texas, a generic insurance law requires auto insurance companies to set rates that are “reasonable, adequate, not discriminatory, and not excessive.” To win approval from the insurance commission, any rate that a company wants to set based on age or gender "must be based on sound actuarial data,” said Ben Gonzalez, spokesman for the Texas Department of Insurance.

That, in practice, allows the companies to consider gender and age when setting rates, he said, as long as they can prove actuarial differences.

“If a company sets a higher rate for a certain age group or gender versus another, it would have to provide information demonstrating higher claims-losses for those customers,” he said, noting that such requests come in “all the time.”

He said the job of the department is to ensure rate changes are justified by the industry data provided. Under Texas law, the new rates are able to go into effect while they are being reviewed, he said, and could be rolled back if the department finds they are not justified.

“Companies must be able to provide data supporting their loss experiences,” before the rates are approved, he said.

NEXT STORY: A New Call to Scrap Portland’s Unusual Form of Government